Cashback

1%On purchases^

Cashback Rewards Credit Card

A better way to get rewarded with 1% cashback on everyday purchases. ^

Check your credit limit without impacting your credit score before you apply

Skip complicated airline points programs. Get 1% cashback on daily spend like groceries, transport and coffee. Cashback is capped at 1% of your credit limit each month.

Cashback is added straight to your account balance each month when you make your minimum repayment on time. No conditions or expiry periods to worry about.

Includes mobile phone insurance, purchase protection and ticket cover when you pay (in full) using your MONEYME Cashback Rewards Credit Card. 1

Skip complicated airline points programs. Get 1% cashback on daily spend like groceries, transport and coffee. Cashback is capped at 1% of your credit limit each month.

Cashback is added straight to your account balance each month when you make your minimum repayment on time. No conditions or expiry periods to worry about.

Includes mobile phone insurance, purchase protection and ticket cover when you pay (in full) using your MONEYME Cashback Rewards Credit Card. 1

Enjoy cashback on everyday purchases with up to 44 days interest free

Cashback

Interest-free

Annual fee

Interest rate

Pay your phone bill with your card and get cover for theft or damage. Up to $1,500 each year (with a $900 cap per claim).1

Covered for undelivered, damaged or incomplete orders when you pay using your Cashback Rewards Credit Card. Also includes accidental damage or theft cover on purchases (annual cap $750).1

Pay with your card and get reimbursed if you cannot attend an event due to unexpected situations like illness or accidents (conditions apply). Up to $1,200 per year.1

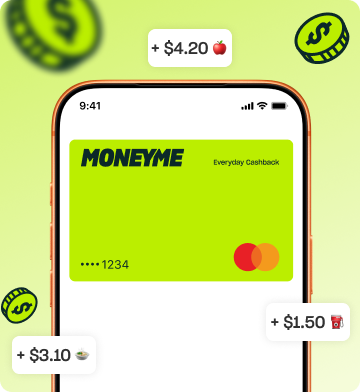

The MONEYME Cashback Rewards Credit Card is designed for simple, everyday spending with real value built in. Apply online in minutes and, if approved, start using your digital credit card straight away with Apple Pay or Google Pay.

With up to 44 days interest free on everyday purchases, this credit card gives you the flexibility to manage your spending while staying in control. You can also earn cashback on eligible purchases, credited directly to your account, so you get rewarded without the complexity of airline points.

Everything is managed in the MONEYME app, from tracking transactions to making repayments, giving you a fast and seamless digital experience.

Used responsibly, a credit card can help you manage cashflow and pay for purchases in a way that suits your budget.

The MONEYME Cashback Rewards Credit Card includes built-in protections designed for everyday spending, so you get more value from the purchases you already make (when you pay in full using your card).

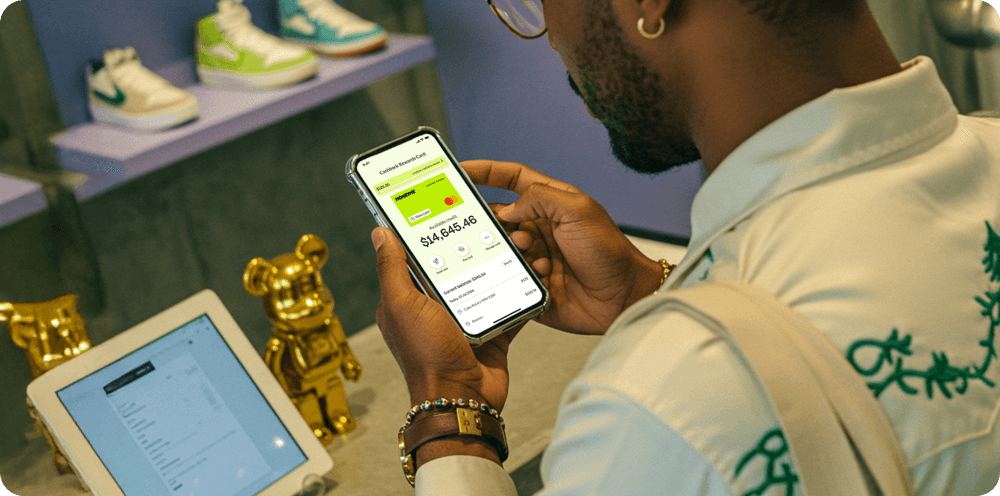

Apple Pay makes everyday purchases with your MONEYME card seamless. Whether you're making a morning coffee run or shopping for a pair of fresh new kicks. Just look for ![]() or the contactless symbol at check-out.

or the contactless symbol at check-out.

Award-winning lender

Quick and efficient service, will definitely be recommending MONEYME to friends and family!

Quick, easy and hassle free! I was pleasantly surprised how easy the process was. Also being able to make extra repayments and payout the loan early without penalty, is a big bonus. Recommended!

Easy to deal with and open about the odds and ends of the deal on the purchase. I will continue using MONEYME for any future purchases for the simple reason of not having to deal with all the issues the big banks have with a purchase. Great work Eujin.

Excellent Customers service, super fast and easy application with the response within hrs.

Approval was fast and even the car dealership was blown away by the speed and ease of dealing with MONEYME. I had my new car in no time! Highly recommend!

MONEYME is one of the best finance companies I've ever gone through great people and what a fantastic service they provide. MONEYME definitely goes above and beyond to satisfy their customers, thank you so much I would highly recommend MONEYME to anyone Australia wide.

A fantastic experience of getting the right finance for my new vehicle. No fuss, no problems, a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

They made the whole experience from start to finish stress free and simple for me to understand which was exactly what I needed. They were just so quick and efficient, the only waiting was with the car yard itself. I would use MONEYME again. I highly recommend them to anyone wanting quick approval at a great rate with fantastic service.

Super quick approval and great interest rate. Money was in the bank within minutes of me accepting the offer. Overall great experience.

Every part of the way i had ongoing communication and I knew where I was at every stage. I was able to sign all documents online. The contract was easy to read and understand. The app is very easy to navigate with a easy to find phone number if i ever need assistance.

Great interest compared to other loans. No hidden costs. Fast and efficient.

No fuss, no problems a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

MONEYME has been so easy to navigate the website and the app, always in contact every step of the application. They gave me a chance to get my family a new car. Great company, fair prices, 100%

I have used MONEYME a few times as they are simple and efficient. Response time is super quick and the rates are competitive. I was on a crazy rate with a credit card company and used MONEYME to consolidate that debt and reduce my repayments.

We had a wonderful experience with MONEYME, fast service and very professional, we will definitely be using them again!

Quick and efficient service, will definitely be recommending MONEYME to friends and family!

Quick, easy and hassle free! I was pleasantly surprised how easy the process was. Also being able to make extra repayments and payout the loan early without penalty, is a big bonus. Recommended!

Easy to deal with and open about the odds and ends of the deal on the purchase. I will continue using MONEYME for any future purchases for the simple reason of not having to deal with all the issues the big banks have with a purchase. Great work Eujin.

Excellent Customers service, super fast and easy application with the response within hrs.

Approval was fast and even the car dealership was blown away by the speed and ease of dealing with MONEYME. I had my new car in no time! Highly recommend!

MONEYME is one of the best finance companies I've ever gone through great people and what a fantastic service they provide. MONEYME definitely goes above and beyond to satisfy their customers, thank you so much I would highly recommend MONEYME to anyone Australia wide.

A fantastic experience of getting the right finance for my new vehicle. No fuss, no problems, a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

They made the whole experience from start to finish stress free and simple for me to understand which was exactly what I needed. They were just so quick and efficient, the only waiting was with the car yard itself. I would use MONEYME again. I highly recommend them to anyone wanting quick approval at a great rate with fantastic service.

Super quick approval and great interest rate. Money was in the bank within minutes of me accepting the offer. Overall great experience.

Every part of the way i had ongoing communication and I knew where I was at every stage. I was able to sign all documents online. The contract was easy to read and understand. The app is very easy to navigate with a easy to find phone number if i ever need assistance.

Great interest compared to other loans. No hidden costs. Fast and efficient.

No fuss, no problems a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

MONEYME has been so easy to navigate the website and the app, always in contact every step of the application. They gave me a chance to get my family a new car. Great company, fair prices, 100%

I have used MONEYME a few times as they are simple and efficient. Response time is super quick and the rates are competitive. I was on a crazy rate with a credit card company and used MONEYME to consolidate that debt and reduce my repayments.

We had a wonderful experience with MONEYME, fast service and very professional, we will definitely be using them again!

Quick and efficient service, will definitely be recommending MONEYME to friends and family!

Quick, easy and hassle free! I was pleasantly surprised how easy the process was. Also being able to make extra repayments and payout the loan early without penalty, is a big bonus. Recommended!

Easy to deal with and open about the odds and ends of the deal on the purchase. I will continue using MONEYME for any future purchases for the simple reason of not having to deal with all the issues the big banks have with a purchase. Great work Eujin.

Excellent Customers service, super fast and easy application with the response within hrs.

Approval was fast and even the car dealership was blown away by the speed and ease of dealing with MONEYME. I had my new car in no time! Highly recommend!

MONEYME is one of the best finance companies I've ever gone through great people and what a fantastic service they provide. MONEYME definitely goes above and beyond to satisfy their customers, thank you so much I would highly recommend MONEYME to anyone Australia wide.

A fantastic experience of getting the right finance for my new vehicle. No fuss, no problems, a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

They made the whole experience from start to finish stress free and simple for me to understand which was exactly what I needed. They were just so quick and efficient, the only waiting was with the car yard itself. I would use MONEYME again. I highly recommend them to anyone wanting quick approval at a great rate with fantastic service.

Super quick approval and great interest rate. Money was in the bank within minutes of me accepting the offer. Overall great experience.

Every part of the way i had ongoing communication and I knew where I was at every stage. I was able to sign all documents online. The contract was easy to read and understand. The app is very easy to navigate with a easy to find phone number if i ever need assistance.

Great interest compared to other loans. No hidden costs. Fast and efficient.

No fuss, no problems a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

MONEYME has been so easy to navigate the website and the app, always in contact every step of the application. They gave me a chance to get my family a new car. Great company, fair prices, 100%

I have used MONEYME a few times as they are simple and efficient. Response time is super quick and the rates are competitive. I was on a crazy rate with a credit card company and used MONEYME to consolidate that debt and reduce my repayments.

We had a wonderful experience with MONEYME, fast service and very professional, we will definitely be using them again!

Check your eligibility in minutes with no impact to your credit score

Apply in minutes and manage your account wherever and whenever you need it.

At MONEYME, we're not just here to provide low rate loans - we're here to make a difference. We believe in providing smart, responsible lending that keeps you financially on track, whilst doing good for the planet.

As a Certified B CorporationTM we're big on sustainability. We hold ourselves accountable to the high standards of the B Corp movement, supporting renewable energy projects, doing our part for the community, and striving towards a greener future.

Explore our impactWe sponsor a child on behalf of every Australian employee. All of these children live in the same community in Uganda, called Busakira.

1 Mobile phone, purchase and ticket protection insurance is underwritten and issued by AIG Australia Limited ABN 93 004 727 753, AFSL 381 686 (AIG) under a group policy of insurance issued to Mastercard. In arranging the insurance, Mastercard acts a group purchasing body under ASIC Corporations (Group Purchasing Bodies) Instrument 2018/751. Eligible persons who can access these insurances are the current holders of a MONEYME Cashback Rewards Credit Card which entitles them to these insurance benefits. You should read the Mastercard Plus Products Insurance Terms and Conditions for mobile phone protection, purchase protection and ticket protection. Eligible persons can claim as third-party beneficiaries by virtue of the operation of s48 of the Insurance Contracts Act 1984. Conditions, exclusions and limits apply to this insurance coverage as set out in the Terms and Conditions and any insurance document provided to the eligible persons, which both may be amended from time to time. MONEYME Financial Group Pty Ltd does not guarantee this insurance. It does not hold an Australian Financial Services Licence and is not authorised to provide financial advice in relation to the insurance. You should consider obtaining your own advice as to the suitability of the insurance coverage for you.

2Conditions apply to the interest free period. Refer to the Terms and Conditions for the Account for further information. After the interest free period, an interest rate of 19.99% p.a. to 26.99% p.a. will apply.

3The actual rate that you receive will depend on a range of factors, including your credit score.

4Applications and maximum credit limits are subject to eligibility criteria including credit approval. Other terms and conditions may apply.

MONEYME acknowledges Aboriginal and Torres Strait Islander peoples as the first people and Traditional Custodians of the land and waterways throughout Australia. We recognise their continued connection to culture, community and Country, and pay our respects to Elders past and present. Learn more about our commitment here.

Our business hours

Sydney/Melbourne time

Customers

Monday - Friday

8AM-7PM

Saturday

9AM-6PM

Sunday

Closed

Partners

Monday - Friday

8AM-5PM

Saturday & Sunday

9AM-3PM

Customer support

Copyright 2026 l MoneyMe Financial Group Pty Ltd l ABN 40 163 691 236 l Australian credit licence number 442218 | Credit criteria, fees, charges, terms and conditions apply.